Timing the Market vs. Time in the Market

Disclaimer: This is only for people who can’t predict the future

"Time in the Market" versus "Timing the Market" is a classic debate in investing. Both strategies are about managing when and how you buy and sell assets, but they differ significantly in approach, risk, and historical success. Here’s our take.

Time in the Market

The idea behind "Time in the Market" is that staying invested over the long term—despite market volatility —tends to produce better returns than trying to time the market and predict its movements. The key idea is that, over time, markets have historically trended upwards despite short-term drops, and by remaining invested, you capture the long-term growth trend.

Why Time in the Market is a Prudent Strategy:

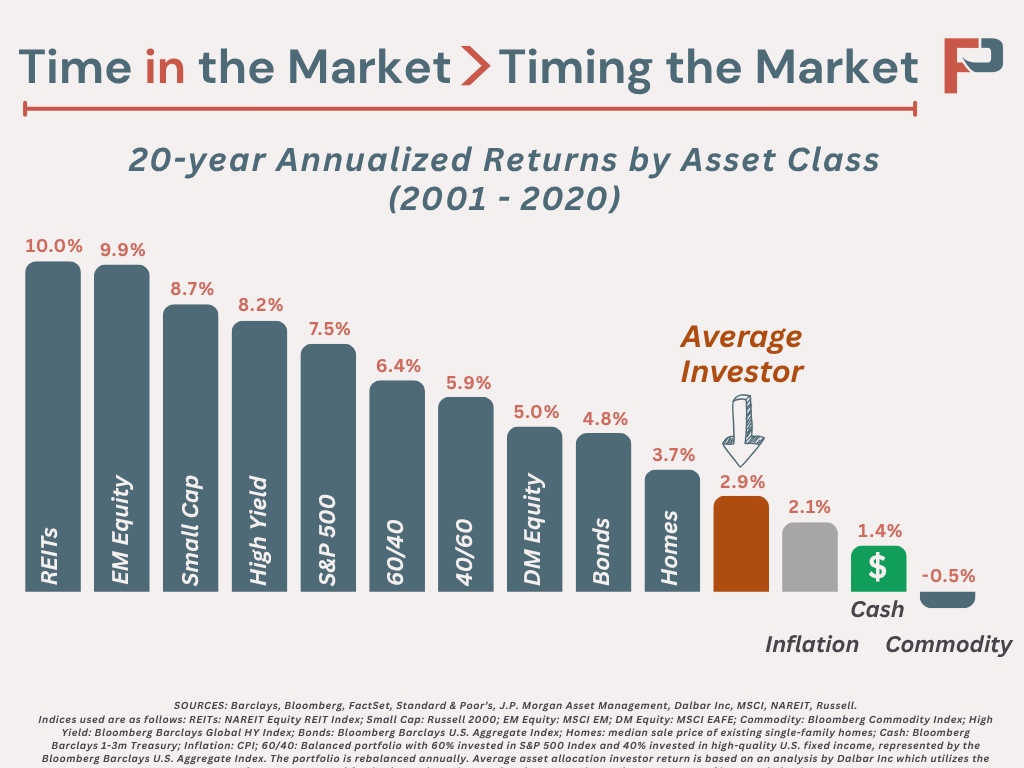

Historical Data: Over the long term, markets generally trend upward due to economic growth, technological advancements, inflation, and corporate profitability.

Compounding Returns: By staying invested, investors can benefit from compounding, where they earn returns not just on the original investment but also on the returns they have already earned.

Avoid Missing Out: Some of the market's best-performing days happen during periods of high volatility or downturns. If you try to time the market, you risk missing out on these big gains.

Lower Costs: Time in the market generally involves less frequent buying and selling, reducing transaction costs and tax liabilities from capital gains.

Lower Stress: With a more hands-off approach, you can feel comfortable “riding the wave” knowing you’ve invested based on principles and logic rather than ambiguity and emotion.

Let's compare two hypothetical investors:

Investor A invests into a position and holds for 20 years with little-to-no intervention.

Investor B tries to "time the market," buying and selling based on short-term predictions.

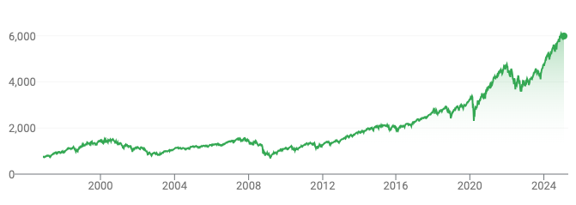

If we look at an index like the S&P 500, which has historically delivered an average annual return of around 6–8% above inflation, Investor A benefits from the long-term trend, while Investor B, trying to time the market, might miss out on key gains during periods of volatility.

The S&P 500 from 2000 to 2020 showed periods of significant volatility (like the 2008 financial crisis), but overall, the market's trend was upward. Someone who stayed invested through the crashes saw strong returns. On the other hand, someone who pulled out during downturns and only got back in later likely missed key recovery periods.

Timing the Market

"Timing the Market" is the idea of trying to buy when the market is low and sell when it is high, based on market predictions, trends, or economic signals. It’s much more about trying to predict short-term price movements.

Why Timing the Market is Risky:

Difficult to Predict: Predicting the market’s movements accurately is incredibly difficult. Even professional fund managers with access to vast resources struggle to time the market effectively.

Psychological Pitfalls: Investors who try to time the market often react emotionally to market swings. When markets drop, they panic and sell; when markets rise, they get greedy and buy in at the peak, leading to poor decisions.

Costs: Active trading can incur high transaction costs, both in terms of commissions and taxes (capital gains), which erode profits.

Examples:

If you had sold your stock in the S&P 500 during the 2008 financial crisis, you would have missed a huge rally in the years following. Even if you "waited" for the market to drop to the bottom before buying back in, predicting the exact low point is almost impossible. For instance, the market hit its lowest point in March 2009, but didn’t fully recover until a few years later.

We’ve heard several stories from investors who have been anticipating a downturn in the market and have been sitting in cash for years. The S&P hit a then-all-time-high in January of 2024 when it eclipsed 4,800 for the first time. Then, just one year later, it reached 6,100 – a staggering 27% gain. At the time of this update (June 24, 2026), the S&P sits at 7,413 — having risen an additional ~21.65% since June 2025.

Statistical Illustration: The Impact of Missing Top Days

One of the most compelling arguments for time in the market comes from research showing how much missing just a few of the best days can drastically impact your returns.

Example: Let’s assume a $10,000 investment in the S&P 500 from 1990 to 2020:

Investment Growth (Without Missing Days): $10,000 grows to about $140,000.

Miss the Best 10 Days: If you missed just the 10 best days during this 30-year period, that same $10,000 investment would have only grown to about $80,000.

Miss the Best 20 Days: Missing the best 20 days reduces growth to around $50,000.

This shows how missing out on key market recoveries during volatile periods can result in significantly lower returns over the long term.

Why "Time in the Market" Works

Markets are volatile in the short term, but over long periods (decades), they generally reflect the overall growth of the economy. A few key points:

Economic Growth: Over long periods, economies grow, leading to increased corporate earnings and higher stock prices.

Inflation: While inflation erodes the purchasing power of money, it also drives nominal prices up over time.

Technological Advancements: Innovation often leads to new industries, higher productivity, and opportunities for growth - just look at what’s happened in tech over the last 10 years!

Because of these factors, time in the market allows you to ride the growth of the economy and benefit from compound growth, reducing the risks of short-term volatility.

Our Take

The reason "Time in the Market" is a more prudent investment strategy than "Timing the Market" is due to its reliance on long-term growth trends, the difficulty of predicting short-term market movements, and the power of compounding. By staying invested, you minimize the risk of missing the market’s best days, avoid emotional decisions, and benefit from the overall upward trend of the economy over time.

TL;DR: "Time in the market" takes advantage of long-term growth and compounding, while "timing the market" is a high-risk exercise in frustration and futility.

Note: Long-term investing is not a zero-sum game. Investment strategies should be well-thought-out and tailored to each individual to reflect their goals and time horizons.

More resources on Market Timing:

Schwab – Does Market Timing Work?

Capital Group – Time, Not Timing

Franklin Templeton – Time vs. Timing in the Market